.svg)

Emergency Funds for Entrepreneurs: Why Every Small Business Needs a Safety Net

Plan your expenses and deductions strategically each year

Egestas tincidunt ipsum in leo suspendisse turpis ultrices blandit augue eu amet vitae morbi egestas sed sem cras accumsan ipsum suscipit duis molestie elit libero malesuada lorem ut netus sagittis lacus pellentesque viverra velit cursus sapien sed iaculis cras at egestas duis maecenas nibh suscipit duis litum molestie elit libero malesuada lorem curabitur diam eros.

- Morbi fringilla molestie magna sed dictum. Praesent pharetra turpis augue.

- Cras mi purus, viverra vitae felis sit amet, tincidunt fringilla lorem.

- non mattis urna ex nec sem. Donec varius diam et suscipit venenati proin tincidunt

- Quisque euismod posuere lacus sit amet volutpat. Praesent vel imperdiet

Maintain accurate and organized financial records for easy reporting

Tincidunt pharetra at nec morbi senectus ut in lorem senectus nunc felis ipsum vulputate enim gravida ipsum amet lacus habitasse eget tristique nam molestie et in risus sed fermentum neque elit eu diam donec vitae ultricies nec urna cras congue et arcu nunc aliquam at.

Talk to a tax professional for expert guidance

At mattis sit fusce mattis amet sagittis egestas ipsum nunc scelerisque id pulvinar sit viverra euismod. Metus ac elementum libero arcu pellentesque magna lacus duis viverra pharetra phasellus eget orci vitae ullamcorper viverra sed accumsan elit adipiscing dignissim nullam facilisis aenean tincidunt elit. Non rhoncus ut felis vitae massa mi ornare et elit. In dapibus.

- Morbi fringilla molestie magna sed dictum. Praesent pharetra turpis augue.

- Cras mi purus, viverra vitae felis sit amet, tincidunt fringilla lorem.

- non mattis urna ex nec sem. Donec varius diam et suscipit venenati proin tincidunt

- Quisque euismod posuere lacus sit amet volutpat. Praesent vel imperdiet

Personalized Marketing: AI helps in analyzing customer data to create personalized marketing campaigns

At mattis sit fusce mattis amet sagittis egestas ipsum nunc. Scelerisque id pulvinar sit viverra euismod. Metus ac elementum libero arcu pellentesque magna lacus duis viverra. Pharetra phasellus eget orci vitae ullamcorper viverra sed accumsan. Elit adipiscing dignissim nullam facilisis aenean tincidunt elit. Non rhoncus ut felis vitae massa. Elementum elit ipsum tellus hac mi ornare et elit. In dapibus.

“Amet pretium consectetur dui aliquam. Nisi quam facilisi consequat felis sit elit dapibus ipsum nullam est libero pulvinar purus et risus facilisis”

Use accounting and tax software to make management easier

Placerat dui faucibus non accumsan interdum auctor semper consequat vitae egestas malesuada quam aliquam est ultrices enim tristique facilisis est pellentesque lectus ac arcu bibendum urna nisl pharetra bibendum felis senectus dolor commodo quam elementum sapien suscipit qat non elit sagittis aliquam a cursus praesent diam lectus tellus mi lobortis in amet ac imperdiet feugiat tristique nulla eros mauris id aenean a sagittis et pellentesque integer ultricies sit non habitant in cras posuere dolor fames.

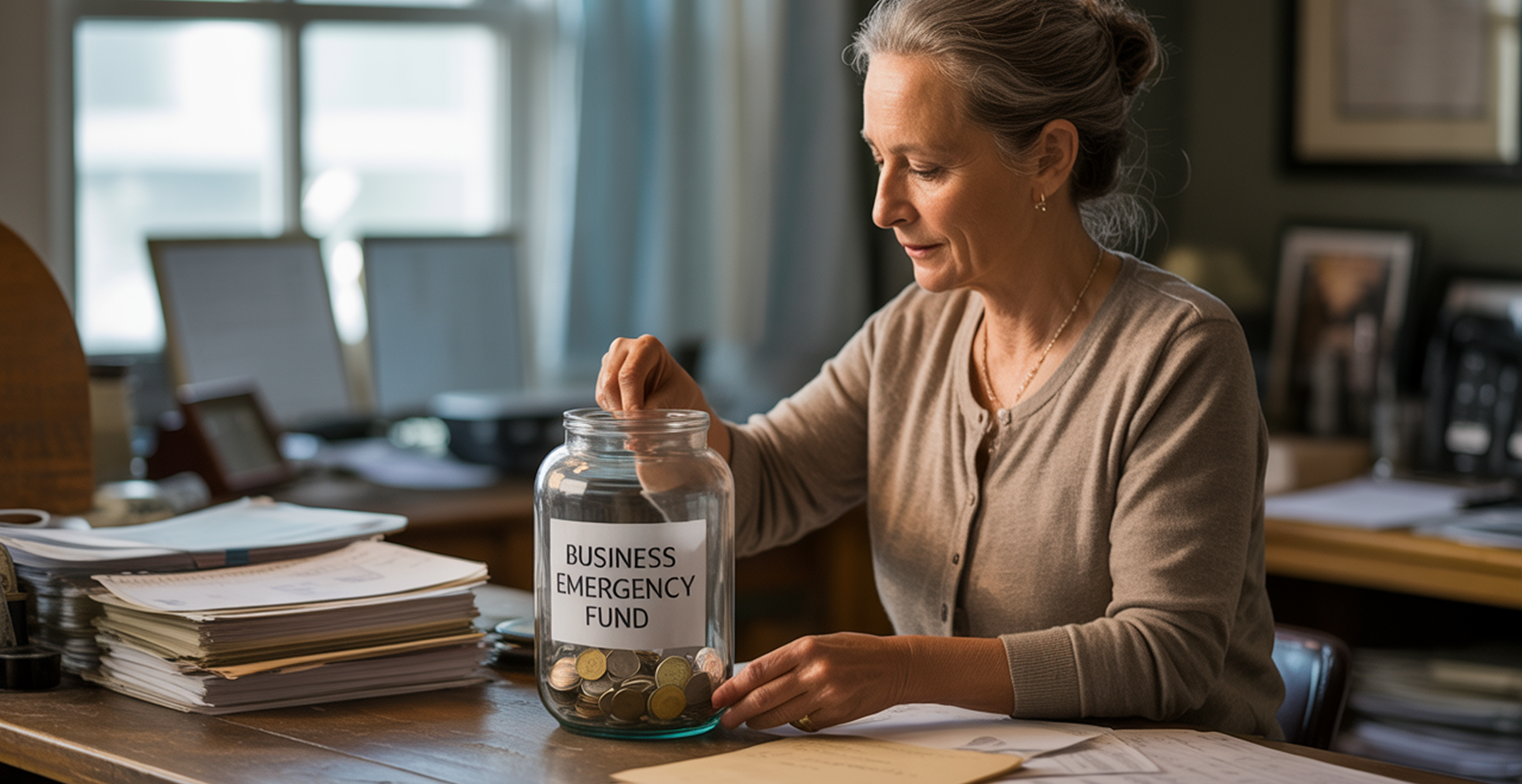

Your Business Emergency Fund: How Much, Where to Keep It, and How to Build It Fast

When unexpected challenges hit—from equipment breakdowns to slow-paying clients—small businesses without a financial cushion can struggle to stay afloat. An emergency fund acts as your company’s safety net, protecting payroll, rent, and critical operations when cash gets tight.

Why Every Small Business Needs an Emergency Fund

- Bridges revenue dips during slow seasons or delayed receivables

- Covers surprise costs (repairs, supply shortages, compliance fees)

- Reduces reliance on debt and high-interest credit cards

- Creates calm and confidence for owners and teams

How Much Should You Save?

Use this simple framework:

- Baseline goal: 1 month of essential operating expenses (for micro/early businesses)

- Standard goal: 3–6 months of essential operating expenses (most small businesses)

- Stretch goal: 6–9 months if you’re seasonal, have client concentration, or volatile sales

What counts as “essential” expenses?

Fixed costs (rent, utilities, insurance, software), plus the minimum variable costs required to keep the doors open (core payroll, baseline inventory, shipping).

Quick formula:

Target Reserve = Average Monthly Essential Expenses × 3–6

Example:

If your essentials average $18,000/month, target $54,000–$108,000.

Where to Keep Your Emergency Fund

- Separate business savings/MM account (avoid spending temptation)

- FDIC/NCUA-insured where applicable

- High-yield savings or treasury/money market for liquidity

- Optional CD “ladder” for a portion you won’t need for 3–12 months

Avoid parking the fund in volatile investments. Safety and liquidity beat yield here.

Practical Steps to Build One (and Stick With It)

1) Start Small—But Start Now

Commit a fixed amount or a percentage of cash inflows (e.g., 2–5% of monthly revenue). Increase the percentage as profits grow.

2) Automate Contributions

Set a recurring transfer the day revenue hits. Treat the reserve like a non-negotiable bill.

3) Capture “Found Money”

Direct tax refunds, one-time rebates, off-season spikes, or surplus cash from cost cuts straight into the fund.

4) Improve Cash In, Slow Cash Out

- Invoice immediately; offer small early-pay incentives

- Tighten collections and follow-ups

- Negotiate longer vendor terms or early-pay discounts (run the math)

5) Replenish After Use—Fast

If you dip into the fund, set a rebuild plan (e.g., 10–20% of monthly profit until back to target).

Clear Rules for When to Use the Fund

Create a simple written policy so decisions are consistent:

- Allowed uses: emergency repairs, essential equipment replacement, short-term revenue shocks, insurance deductibles

- Not for: routine shortfalls, growth projects, owner distributions

- Approval: define who authorizes withdrawals and how they’re documented

Pair Your Fund with Risk Protection

- Business interruption & property insurance: the fund covers deductibles and waiting periods

- Line of credit: secondary back-up for larger disruptions (set it up before you need it)

- Contingency planning: identify alternative suppliers and critical spares for fast recovery

Monitor Your Cushion Like a KPI

Track these monthly:

- Months of Runway = Cash / Avg. Monthly Essential Expenses

- Operating Cash Flow trend

- Quick Ratio (Cash + AR) / Current Liabilities

Set alerts if runway drops below your minimum (e.g., 2 months).

Real-World Snapshot

A café with two months of reserves covered payroll and rent through a slow winter without taking on expensive debt. Because the owner had a policy and automated contributions, rebuilding the fund by spring was straightforward.

6-Week Starter Plan (Quick Win)

Week 1: Open a separate savings/MM account; define “essential” expenses

Week 2: Automate a weekly transfer (even $150–$300 to start)

Week 3: Tighten invoicing & collections; cut one low-value subscription

Week 4: Ask top suppliers for Net-45/Net-60 or early-pay discounts

Week 5: Bank any “found money” (refunds, off-cycle wins) into the fund

Week 6: Review progress; set your official reserve target and rebuild rules

Bottom Line

An emergency fund isn’t optional—it’s survival insurance for your small business. Start small, automate contributions, define when you’ll use it, and rebuild quickly after you do. The confidence and stability you gain are worth every dollar you set aside.

Want a tailored reserve target and cash-flow plan based on your numbers? Contact Peak Accounting to get started.

%20B2.png)

%20B-3.png)